Listen to our podcast on this topic here: Podcast: #3 – What Multiple should I use for a Business Valuation?

The problem with this question is that the asker doesn’t always understand that there are different types of multiples designed for different contexts and the word “multiple” means different things in different situations. A multiple can have very different meanings and valuation outcomes depending on the context. I don’t mean that different businesses have different multiples (although they do), I mean that the multiples themselves are derived differently and applied differently to get different valuation components in the result.

There are two broad contexts for multiples used in business valuation theory based on the valuation approach being applied by the valuer. That is, whether the valuer is applying an Income Approach or Market Approach will determine the context of the multiple, how it is derived, what to multiply it by and what to do with the valuation outcome once you get the result.

If you are using an income approach (capitalisation of future maintainable earnings (CFME) or discounted cash flow (DCF)) you are considering the return on investment based on the business cash flows. The multiple in this context is related to the required rate of return on the investment to compensate the capital providers for the risks in the business cash flows.

But if you are using a market approach on the other hand (comparable transaction, guideline public company or rule of thumb) the multiple is derived directly from observations within the data. That is, there is no direct correlation to return on investment and you need to calculate the multiple from the data where you have a numerator (sale price) and a denominator (potentially any level of revenue, profit, cash flow or any other identifiable metric). The multiple is simply the numerator divided by the denominator.

The mistake a lot of valuers make is to use an income approach to value the business but to adopt a multiple derived by comparable data. It’s tempting to do, but when that happens you’ve now got a hybrid method that doesn’t make a lot of sense when you look at the fundamentals that underpin the theory on each valuation method and how they are derived. The cash flows and the multiple in that situation don’t live in the same hypothetical universe.

We’ll start by taking a closer look at the income approach and how the multiple is derived under the various valuation methods that exist under this approach. We’ll concentrate on the capitalisation of future maintainable earnings (CFME) method because it is so popular when valuing small businesses.

Remember that a CFME method is really just a short-form discounted cash flow (DCF) method. Most valuation textbooks lay out the math to prove it, so I won’t do it here. The DCF method typically looks at Operating Cash Flow after Capital (pre-interest, post-tax) for a number of forecast periods. A terminal value is also calculated at the end of the last forecast using any of a few common methods that I won’t go into here other than to note that they all result in another single lumpy cash flow around the time of the last forecast.

A discount rate is then applied to each period’s cash flow (and the terminal value) to punish the cash flows for the time value of money and risk. The present values of each cash flow are summed together to calculate the Enterprise Value (also referred to as the value of the firm amongst other things). The Enterprise Value already includes all operating assets and operating liabilities ordinarily required to operate the core business. Any other non-ordinary assets and liabilities/debts are then added and subtracted to calculate the equity value of the entity. The goodwill (if any) is implied if the Enterprise Value is greater than the ordinary net operating assets.

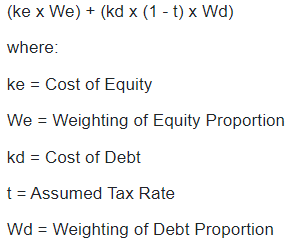

The discount rate in a DCF is typically calculated using a weighted average cost of capital (WACC) because the enterprise value that results is effectively funded by both equity and debt providers. So we need to consider the risks and the required rates of return for both equity and debt providers. Debt providers typically have less risk than equity providers because they get paid first and get paid pre-agreed amounts. Equity providers need to wait for dividends or a surplus (if any) when the company is sold or wound up.

Once we estimate the rate of return for both types of capital, we apply weightings to each in accordance with optimal and sustainable debt/equity levels. More sustainable debt means more weighting is applied to debt providers and a lower weighted average rate of return overall.

The weighted average cost of capital formula is illustrated below:

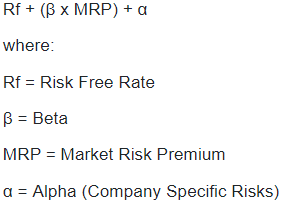

The cost of equity is the rate of return required by equity providers to compensate them for the risks in the cash flows. One common method to calculate the cost of equity is the capital asset pricing model which is illustrated below:

The cost of debt is usually based on a benchmark corporate interest rate or the company’s current borrowing rate. The interest rate is reduced for tax.

Refer to your favourite valuation textbook to go deeper on all the details, I’ve only illustrated an overview here to emphasise how risks largely determine the discount rate.

Now if we go back to the CFME method and think about the multiple and we know it must relate to a DCF discount rate then we can start to see the link. We know that in a DCF the higher the risks the higher the discount rate and the lower the present value (enterprise value). In the CFME method we intuitively know that the higher the risks the lower the multiple. This works because in a CFME method instead of using various forecast periods we pick one single level of profit or cash flow and assume that it is earned in perpetuity. The simple formula for a perpetuity is the cash flow multiplied by 1 / yield.

The yield in this case is the discount rate (calculated as a weighted average cost of capital). In reality we might expect the cash flows to grow over time and this can be factored into the denominator by reducing the discount rate by a constant growth rate. So the final formula ends up being CF x (1 / (r – g)). The effective multiple is everything after the multiplication sign. So you can see that in the CFME method the multiple is the inverse of the discount rate offset by the growth rate. A higher discount rate means a lower multiple. A higher growth rate means a higher multiple.

For example, a discount rate of 25% and a growth rate of 5% would result in a multiple of 5, calculated as 1 / (25% – 5%). The future maintainable earnings are multiplied by 5 to obtain the enterprise value. Surplus assets and surplus liabilities/debts are then adjusted to calculate the total equity value of the company. The implied goodwill (if any) included in the enterprise value is the enterprise value less the ordinary net operating assets.

Whether you are deriving the multiple for a CFME method with this level of detail or just picking a multiple that makes sense, under the hood this is how it works and this is what your multiple is implying.

A key thing to consider when using the CFME method is that you are typically looking backwards at past profits or cash flows, maybe including some forecasts, making normalisation adjustments and applying a weighted average to calculate the future maintainable earnings amount. This is important because you are doing this with the sole purpose of trying to estimate the most likely future cash flows (just like a DCF) but you are doing it by relying heavily on past normalised results. But be clear, this is still a forward-looking valuation process.

If you want to see the CFME and DCF methods in action check out the sample business valuation report.

Now let’s have a look at how a multiple is calculated under a market approach. We will concentrate on a comparable transaction method because it is so popular for small businesses.

A comparable transaction method is often quite simpler than a CFME or DCF method because you just have to gather comparable data, derive the observable multiples and apply them to the subject business. You don’t necessarily have to normalise past results, forecast future results or consider reasonable rates of return on investment. The key is to find comparable data.

Comparable data can come from many sources. You can subscribe to proprietary databases, talk to business brokers and otherwise search online and offline for any business sales evidence. Let’s assume we’re using the popular DealStats database and we’ve found a number of transactions that we think are comparable in size and operations to the business we are valuing.

For each sale transaction in the dataset we need to derive “the multiple”, but in practice we will often derive several multiples for each transaction. DealStats will typically provide us with the price expressed in terms of Market Value of Invested Capital. This can vary between transactions but is often the total of equipment, stock, goodwill and other intangibles. This will be the numerator in our derived multiple. They will also give us several other data points such as last year’s revenue, EBIT, EBITDA, SDE (seller’s discretionary earnings). These will be our denominators. We will end up with four separate multiples: MVIC/Revenue, MVIC/EBIT, MVIC/EBITDA and MVIC/SDE.

Already we can see that even for the one transaction we may have four or more multiples to consider which all have different contexts. We then do the same for each transaction in the dataset and work out the median, mean and harmonic mean. We have to select one of those types of statistics to adopt and if we think it’s appropriate we can then apply subject business specific adjustments to each of the four multiple types to allow for differences between the average transaction and the subject business.

We then apply the subject company’s actual revenue, EBIT, EBITDA and SDE amounts to each of the multiples to get four values for the business. Because we have more than one valuation outcome we would need to adopt one over the others or apply a weighted average across them all to get the value of the business.

Importantly, we have to be very careful to understand and apply the numerator and denominator in each multiple exactly as they were derived. That is, if the denominator in the data source is last year’s unadjusted EBITDA we shouldn’t normalise the subject company’s EBITDA in any way otherwise it is no longer comparable. If the denominator is SDE we need to calculate the subject company’s SDE in exactly the same way.

If the numerator is the sale price that includes equipment, stock, goodwill and other intangibles then when we apply the subject company’s denominator to the multiple we get the same components as the numerator. We can’t add stock on top because it’s already included. In some cases the numerator in the dataset will just be goodwill and in that case you get goodwill directly as a result and have to add everything else on top. The market approach requires an apples and apples comparison and you need to deeply understand the numerator and denominator in each derived multiple so you can apply them correctly.

If you want to see a comparable transaction method in action check out the sample business valuation report.

By now you can appreciate that the word “multiple” is thrown around very loosely and can mean many different things depending on the valuation method being used and how the multiple was specifically derived. Even in a CFME method I might adopt a multiple of say 3.5 to calculate the enterprise value, but the implied goodwill multiple in hindsight might be say 1.5 depending on the level of net operating assets ordinarily used to operate the core business. So the multiple is both 3.5 and 1.5 in the one valuation. Multiple means nothing without the context.

When I get asked about what multiple to use in a business valuation I need to understand the context before I can start to think about a meaningful response so I don’t provide an answer that gets misinterpreted and applied inappropriately. If you are doing a CFME method the multiple results in Enterprise Value and you should consider the risks in the cash flows, the ratio of equity/debt and the growth rate. If you take a sneaky peak at what other business are selling for that’s up to you. If you are doing a comparable transaction method you need to find comparable data and derive and average the multiples after fully understanding the numerator and denominator in each multiple. If you want to adjust the multiple for subject business risks that’s up to you. You then apply the subject company’s actual denominator and get the numerator (and its included components) as a result.

In the Valuation Ultimate software you have full control over the components of each of the valuation methods. If using a CFME method you can choose any level of profit or cash flow and make any normalisation adjustments you wish. You can develop the multiple using a full weighted average cost of capital approach using the CAPM, use a simple buildup or enter a multiple you’ve already decided on. If using a comparable transaction method you can enter business sale transactions with different metrics, choose median, mean or harmonic mean and apply subject company adjustments as you wish. As the valuer you apply your professional judgement at every step. The software is a safe and efficient workspace for you to do your best work.

Want to go deep into valuation theory and hear personal stories from valuation experts, listen to our business valuation podcast.